In this article, we’ll discuss these differences and how they affect you, so you can discover how to avoid potentially costly problems.

Differences

There are four key differences between American- and European-style options:

- Underlying

All optionable stocks and exchange traded funds (ETFs) have American-style options. Among the broad-based indices, only limited indices such as the S&P 100 have American-style options. Major broad-based indices, such as the S&P 500, have very actively traded European-style options.

A few examples of European style options are the S&P 500 Index (SPX), the Russell 2000 Index (RUT), and the Nasdaq (NDX). These are the three most liquid European style options, and that’s why we trade them at NavigationTrading.

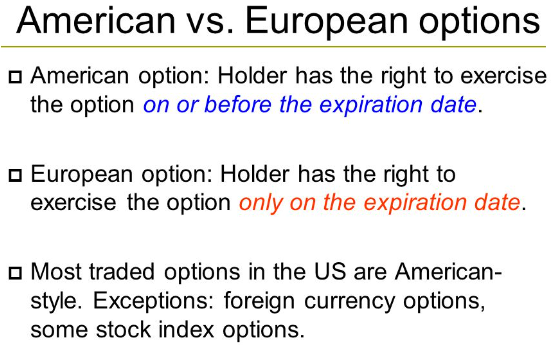

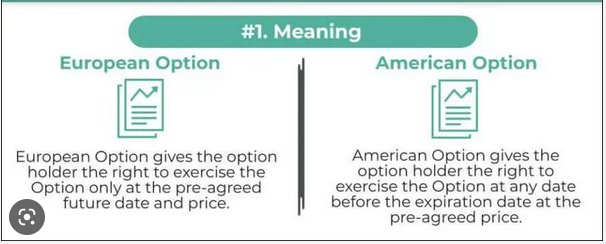

- The Right to Exercise

Owners of American-style options may exercise at any time before the option expires, while owners of European-style options may exercise only at expiration.

- Trading of Index Options

- American index options cease trading at the close of business on the third Friday of the expiration month. (A few options are “quarterlies,” which trade until the last trading day of the calendar quarter, or “weeklies,” which cease trading on Friday of the specified week.)

-

European index options stop trading one day earlier, at the close of business on the Thursday preceding the third Friday.

- Settlement Price

This is the official closing price for the expiration period and establishes which options are in-the-money and subject to auto-exercise. Any option that is in-the-money by 1 cent or more on the expiration date is automatically exercised unless the option owner specifically requests his/her broker not to exercise.

- American index options cease trading at the close of business on the third Friday of the expiration month. (A few options are “quarterlies,” which trade until the last trading day of the calendar quarter, or “weeklies,” which cease trading on Friday of the specified week.)

-

European index options stop trading one day earlier, at the close of business on the Thursday preceding the third Friday.

Here’s how it works:

- On the third Friday of the month, the opening price for each stock in the index is determined. Because individual stocks open at different times, some of these opening prices are determined at 9:30 AM (EST) and others a few minutes later. Some stocks may not begin trading until an hour or two later.

- The underlying index price is calculated as if all stocks were trading at their respective opening prices at the same time. This is not a real-world price, you cannot look at the published index price and assume the settlement price is close in value to any of the early-morning published prices for the index.

Exercise Rights

When you own an option, you control the right to exercise. Occasionally, it may be beneficial to exercise an option before it expires (to collect a dividend, for example), but it’s seldom important.

When you are short an American-style option (you sold the option without owning it) and are assigned an exercise notice before expiration, instead of being short the option, you are now short the stock. Unless your account is too small to carry a short stock position, this is not a problem; and if your account is that small, you should probably not be trading options.

The Easiest Way to Avoid Early Exercise Risk

The only time an early assignment carries any significant risk occurs with American-style, cash-settled index options. So the easiest way to avoid the early exercise risk is to avoid trading American options. When you receive an assignment notice in the morning, you must repurchase that option at the previous night’s intrinsic value. That may place you at serious risk if the market undergoes a significant move, because that forced purchase makes your position different from the one you thought you owned.

Cash Settlement

It’s advantageous to everyone when options are settled in cash:

- American: The settlement price for the underlying asset (stock, ETF, or index) with American-style options is the regular closing price or the last trade before the market closes on the third Friday. After hours trades do not count when determining the settlement price.

- European: It is not as easy to learn the settlement price for European-style options. In fact, the settlement price is not published until hours after the market opens for trading.

Because these cash-settled options are almost always European-style, and assignment only occurs at expiration, the option’s cash value is determined by the settlement price.

Settlement Price

With American-style options, there are seldom any surprises. When the stock is trading at $40.12 a few minutes before the closing bell on expiration Friday, you can anticipate that the 40 puts will expire worthless and that the 40 calls will be in-the-money. If you have a short position in the 40 call and don’t want to be assigned an exercise notice, you can repurchase those calls. The settlement price may change and those 40 calls may move out-of-the-money, but it’s unlikely that the value of those calls will change significantly in the last few minutes.

With European-style options, the settlement price is often a huge surprise, which may prove beneficial to some but a disaster for many others. That’s because when the market opens for trading on the morning of the third Friday, there is often a gap, a significant price change from the previous night’s close. This doesn’t happen all the time, but it happens often enough to turn the apparently low-risk idea of holding that position overnight into a large gamble.

When you own the European option, here’s the situation you face Thursday afternoon, the day before expiration:

- No shares exchange hands.

- You don’t have to be concerned with rebuilding a complex stock portfolio, because you don’t lose your stocks if assigned an exercise notice on calls you wrote, as in covered call writing or a collar strategy.

-

The option owner receives the cash value – and the option seller pays the cash value – of the option. That cash value is equal to the option’s intrinsic value. If the option is out of the money, it expires worthless and has zero cash value.

When short the option, you face a different challenge:

- If the option is almost worthless, holding onto it and hoping for a miracle is not a bad idea. Owners of low-priced options, worth a few nickels or less, have been known to earn hundreds, or even a few thousand dollars, when the market gapped open the following morning. Most of the time those options expire worthless, but an occasional large reward is possible.

- If you own an option that has a significant value – let’s say $1,000 – you have a decision to make. The settlement price could make the option worthless or double its value. Do you want to take that risk? That’s a decision only individual investors can make for themselves.

Taxes

The tax treatment for European style options is a little bit more favorable as they receive the IRS Section 1256 tax treatment. Which means that 60% of the gains can be counted as long term capital gains, which would be at the lower 15% rate. 40% of your profit would be taxed as ordinary income.

American style options are taxed as 100% short term capital gains. Depending on your overall income, and tax bracket, the taxes owed on profits would be added as ordinary income.

Summary

If you decide to trade index options, be certain you understand the differences between American- and European-style options. More importantly, to avoid a significant loss, you must understand how the settlement price of European options is determined. It makes a big difference to how you manage a position, especially when you have a position that includes short options. It’s prudent to stay away from settlement risk by exiting positions—that have little more to gain—no later than Thursday, the last day those options can be traded.

Mark Wolfinger has been in the options business since 1977, when he began his career as a floor trader at the Chicago Board Options Exchange (CBOE). Since leaving the Exchange, Mark has been giving trading seminars as well as providing individual mentoring via telephone, email and his premium Options For Rookies blog. Mark has published four books about options. His Options For Rookies book is a classic primer and a must read for every options trader. Mark holds a BS from Brooklyn College and a PhD in chemistry from Northwestern University.

Related articles

- Option Settlement: The Basics

- Everything You Need To Know About Options Assignment Risk

- How Index Options Settlement Works

- Can Options Assignment Cause Margin Call?

- Assignment Risks To Avoid

- The Right To Exercise An Option?

- Options Expiration: 6 Things To Know

- Early Exercise: Call Options

- Expiration Surprises To Avoid

- Assignment And Exercise: The Mental Block

- Should You Close Short Options On Expiration Friday?

- Fear Of Options Assignment

- Expiration Short Strategies

- What Are Cash-Settled Options?

Original source: https://steadyoptions.com/articles/american-vs-european-options-the-differences-r748/