In an earlier article, we explained why assignment on a covered call is usually not a major concern.

However, some investors prefer to avoid having their shares of stock sold.

They may want to prevent a taxable event triggered by the sale of stock, which can result in either a capital gain or a capital loss.

While taxes are unavoidable, the length of time an investor has held the shares can significantly affect how much tax is owed, as gains may be classified as either short-term or long-term depending on the holding period.

Many investors may want to hold the stock for the long term for that reason, or to continue receiving dividends without having to sell and buy it again (potentially triggering a wash sale).

Contents

-

- Buy Back The Short Call.

- Rolling A Covered As The Price Reaches The Strike Price

- Roll Before Ex-Dividend Dates.

- Roll When The Extrinsic Value Is Low.

- Summary

In this article, we’ll walk through the key method investors can use to avoid having their stock called away in a covered call.

While this applies to ETFs as well, we’ve used the word “stock” to refer to both individual equities and ETFs, since they trade in essentially the same way.

Let’s get into the details with an example.

Buy Back The Short Call.

Let’s say we buy 100 shares of XLE (an energy sector ETF) on January 14, 2026, at $48 per share.

We then immediately sell a call option on XLE with a strike price of $50 that will expire on February 13th, 2026 (just about a month away).

The call option can only be sold after the shares have been bought, not before.

Or the two transactions can occur simultaneously in a single order (which is also known as a “buy write” order), as in the following:

Date: Jan 14, 2026

Price: XLE @ $48.00

Buy 100 shares of XLE at $48.00

Sell to open one contract Feb 13 XLE $50 call @ $0.61

The option contract is quoted on a per-share basis (here, $0.61 per share).

Since one contract represents 100 shares, we collected $61 from the sale of that one call option contract.

This combination of owning stock and selling a call option on that stock is known as a “covered call” because the 100 shares of stock cover the obligation of the short call option.

When a call option is sold, we say that we are “short a call”.

And that option sold is known as a short call.

That option is sold to a buyer of the option.

If the option buyer exercises the option contract, we are obligated to sell 100 shares of XLE at $50 per share (the strike price) – regardless of the market price.

The option buyer can choose to exercise at any time.

However, that call option will automatically be exercised if the stock price exceeds its strike price at expiration.

When the call option is “exercised”, we are “assigned” the stock.

This is what is known as “assignment of a covered call,” and the stock we already own is automatically sold.

On February 13, 2026, the call option is set to expire at the end of that day’s trading session.

Since the price of XLE is at $54.30 per share and is likely to remain above the strike price of $50 going into the market close, this option is likely to be automatically exercised at the market close.

When that happens, our 100 shares of XLE will automatically be sold at $50 per share.

To avoid this, we will close the call option.

Because we sold the call option to open the position, we must buy it to close the position.

By buying back the call option, we will no longer have the short call option.

Without the call option contract, we eliminated our obligation to sell the stock.

Date: Feb 13, 2026

Price: XLE @ $54.30

Buy to close one contract Feb 13 XLE $50 call @ $4.40

This $4.40 is quoted on a per share basis.

So it actually cost us $440 to buy back one contract of the call option.

We definitely lost money on the call option.

Because we collected $61 to sell it.

And now we had to buy it back for $440.

A $379 loss.

But at least we got to keep our 100 shares of XLE, which had appreciated from $48 per share to $54.30 per share.

Gaining $6.30 per share means our 100-share position has profited by $630.

All in all, the covered call trade made a profit of $251.

$630 – $379 = $251

Ideally, we really shouldn’t wait until the last day right before expiration to close the call option.

Since assignment risk is highest in the last week before expiration, many investors will want to exit their call option one week prior to expiration if they really want to avoid assignment.

Rolling A Covered As The Price Reaches The Strike Price

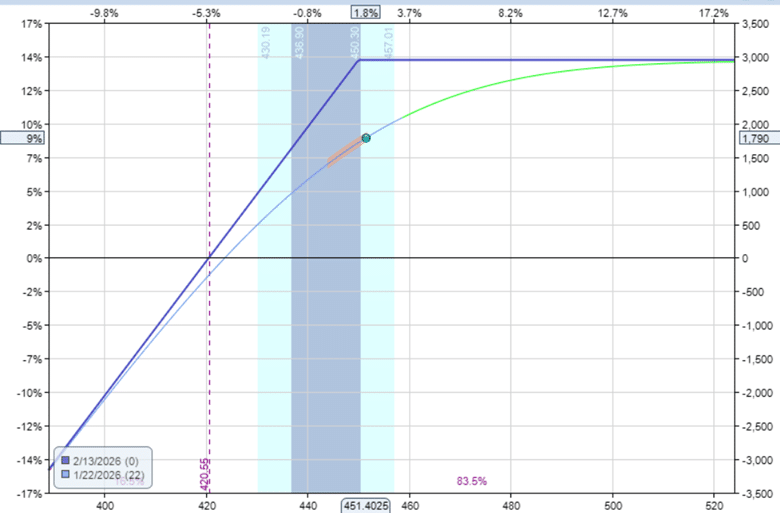

During the same period, suppose we buy 100 shares of gold ETF (GLD) and sell a covered call against it.

Date: Jan 14, 2026

Price: GLD @ $423.90

Buy 100 shares of GLD at $423.90

Sell to open one contract Feb 13 GLD $450 call @ $3.37

Net debit: $42,390 – $337 = $42,053

This would be the payoff graph:

On January 22nd, GLD was already up at $451.40 per share.

It had just gone higher than the strike price of $450.

The call option is now “in-the-money”.

This is because the buyer of the call option can make a profit if he decides to exercise that option now.

The buyer of the option can purchase GLD shares at $450 per share, which is below the market price.

A call option being in-the-money increases the chance that our GLD stock will be called away.

Therefore, we roll the call option.

Rolling a call option means closing the existing option and then selling a new one with a different strike price and expiration date.

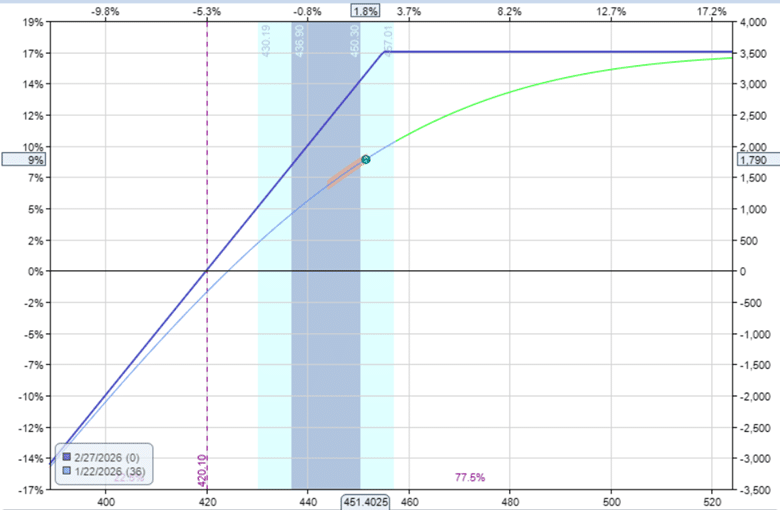

Date: Jan 22, 2026

Price: GLD @ $451.40

Buy to close one contract Feb 13 GLD $450 call @ $12.98

Sell to open one contract Feb 27 GLD $455 call @ $13.60

Net credit: $62

Now the new strike price of the call option is at $455, and the new expiry is on February 27th.

The payoff graph after the roll looks like this…

We had increased the profit potential of the covered call and given more room for the stock price to rise before the call option goes in-the-money again.

Roll Before Ex-Dividend Dates.

Another reason to roll a call option is prior to ex-dividend dates, when there is a greater chance that a stock will be called away.

This is because other investors want to own the stock before the ex-dividend date to receive the dividend.

And they may exercise their call option to obtain that stock (even if the call option is not in the money).

Consider the following covered call on Target (TGT), initiated on January 2nd, when it is trading at exactly $100 per share.

Date: Jan 2, 2026

Price: TGT @ $100.00

Buy 100 shares of TGT at $100.00

Sell to open one contract Feb 20 TGT $115 call @ $0.78

On the morning of February 10th, TGT had risen to $114.36 per share.

While it is not in the money yet, this stock has a good chance of being called away because it is one day before Target’s ex-dividend date.

Any investor who wants to collect Target’s $1.14 per share dividend must own the stock prior to the ex-dividend date.

The investor to whom we sold the call option might exercise it to obtain the stock.

He might exercise to buy TGT at $115 per share even when the market price is slightly lower at $114.36.

Because by doing so, he knows that he will receive $1.14 per share on the dividend payment date.

He would still profit by $0.50 per share.

$114.36 + $1.14 = $115.50

If he exercises his option, we will be assigned on the call option, and our 100 shares of TGT will be sold at $115 per share.

If we want to avoid assignment and don’t want to sell our share (because we probably want the dividend ourselves), we need to close or roll the call option before another investor exercises it.

And it need not be one day before ex-dividend; it could be a week before ex-dividend or whenever the math makes sense.

Roll When The Extrinsic Value Is Low.

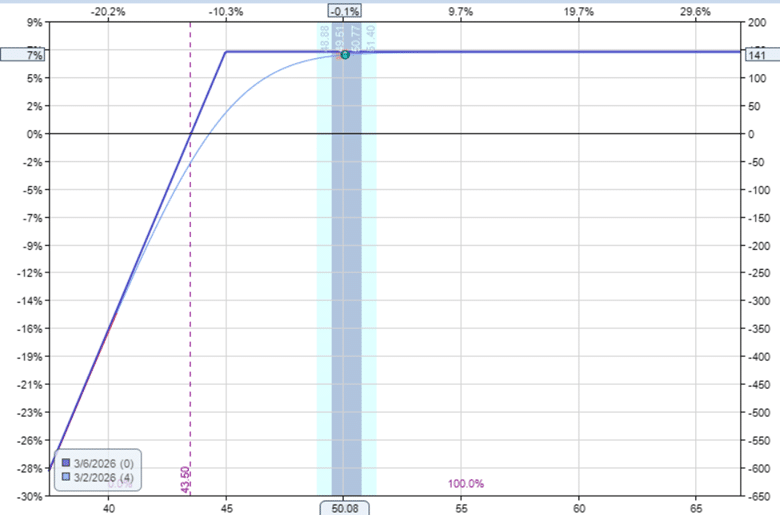

In this last example:

Date: Feb 2, 2026

Price: VZ at $44.21

Buy 100 shares of VZ at $44.21

Sell to open one contract Mar 6 VZ $45 call @ $0.67

We sold a covered call at a strike price of $45 when VZ is trading at $44.21.

We collected $0.67 per share on this option, or $67 per contract.

The value of this option is purely extrinsic value.

This option currently has no intrinsic value since it is completely out of the money.

Now you have to think from the perspective of the buyer who bought our call option.

He bought the option even though it has no current intrinsic value.

The option without any intrinsic value means that if the owner exercised it now, he would not make any money.

The buyer bought the option from us for its extrinsic value.

Extrinsic value represents the potential that the option can go in-the-money sometime in the future before expiration.

And the buyer hopes that this happens.

Well, it happened.

VZ just skyrocketed, and on March 2nd, it was already at $50.08 per share, way past the $45 strike price, and still has 4 days till expiration.

This means that the call option is deep in the money.

The value of the call option has ballooned to $5.12 per share.

The value of this option is mostly intrinsic value now.

The intrinsic value is calculated to be $5.08 per share:

$50.08 – $45.00 = $5.08

That means there is only $0.04 per share of extrinsic value left in the option – very little potential remaining.

It makes sense for the call option holder to exercise early and lock in a profit by buying 100 shares at $45 per share when the option is trading at $50.08 per share.

The point is that when the option we sold is in-the-money and has very little extrinsic value remaining, there is a chance it will be exercised.

From our perspective, this typically happens when the covered call has already made most of its profits…

And it is time to roll the call up to increase upside potential and to avoid assignment.

Summary

If you do not want the shares in your covered call position to be called away, monitor the trade and roll proactively.

While technically speaking, the stocks can be called away at any time, four scenarios increase the likelihood of being assigned:

- Near expiration

- Call option is in-the-money

- Near ex-dividend dates

- When extrinsic value is low

Once your stock is called away, the shares are gone.

While you can always buy them back in the open market, brokers will not necessarily warn you before early assignment, nor allow you to decline an assignment, nor reverse it after it happens.

For this reason, proactive management and timely rolling are essential if you want to avoid losing your shares.

We hope you enjoyed this article on avoiding assignment in covered calls.

If you have any questions, please send an email or leave a comment below.

Trade safe!

Disclaimer: The information above is for educational purposes only and should not be treated as investment advice. The strategy presented would not be suitable for investors who are not familiar with exchange traded options. Any readers interested in this strategy should do their own research and seek advice from a licensed financial adviser.

Original source: https://optionstradingiq.com/how-to-avoid-assignment-on-covered-calls/