Let’s start by running a scan on stocks reporting earnings this week, which includes the total option volume indicator, sorted from greatest to least.

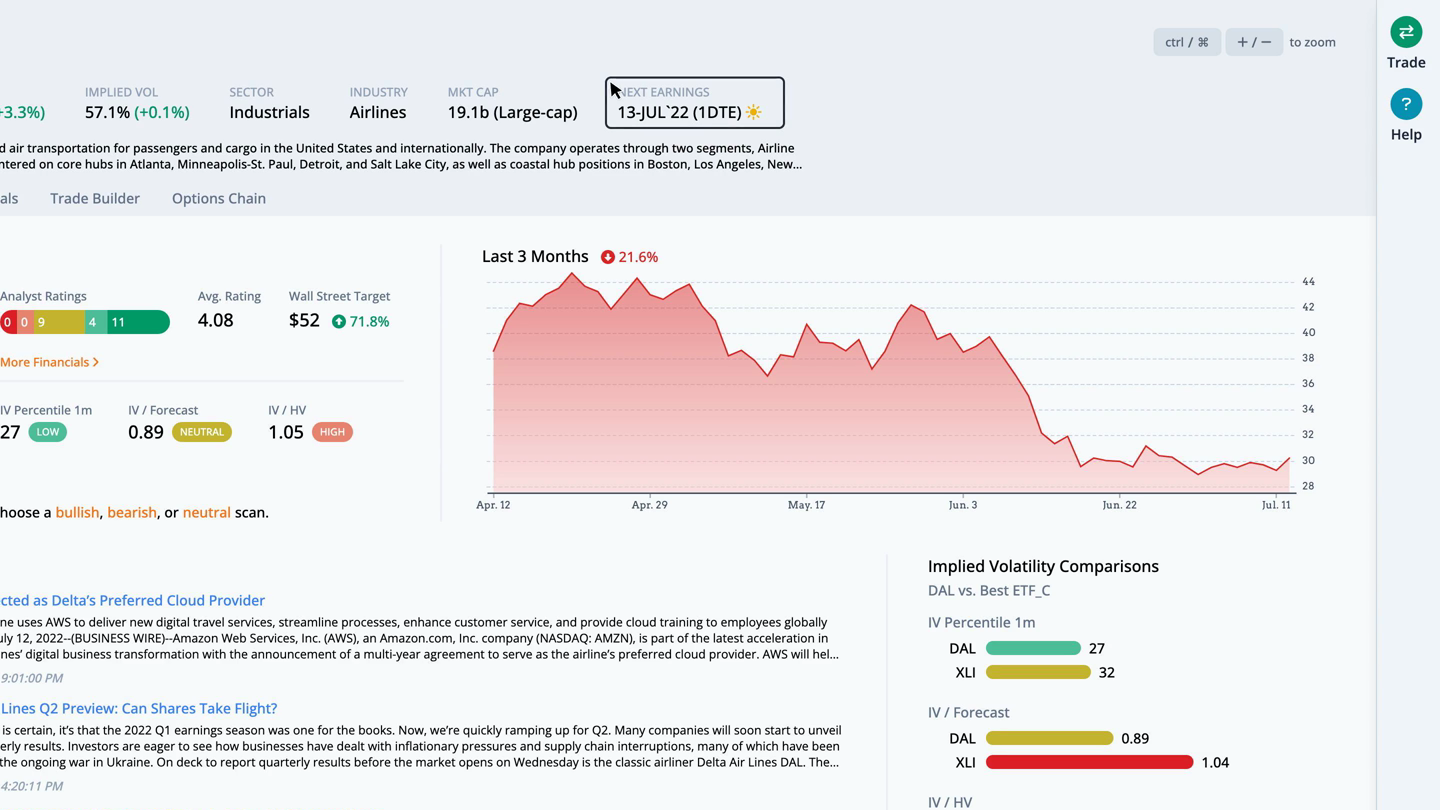

Focusing on Delta Air Lines (DAL), as we click through, we see this large-cap company in the airlines industry reports earnings on Wednesday, July 13th, after the close.

The earnings and financials tab takes us to more detail showing the options market expecting a move of 6.8% in either direction. This move was breached in 0 out of the last 12 earnings.

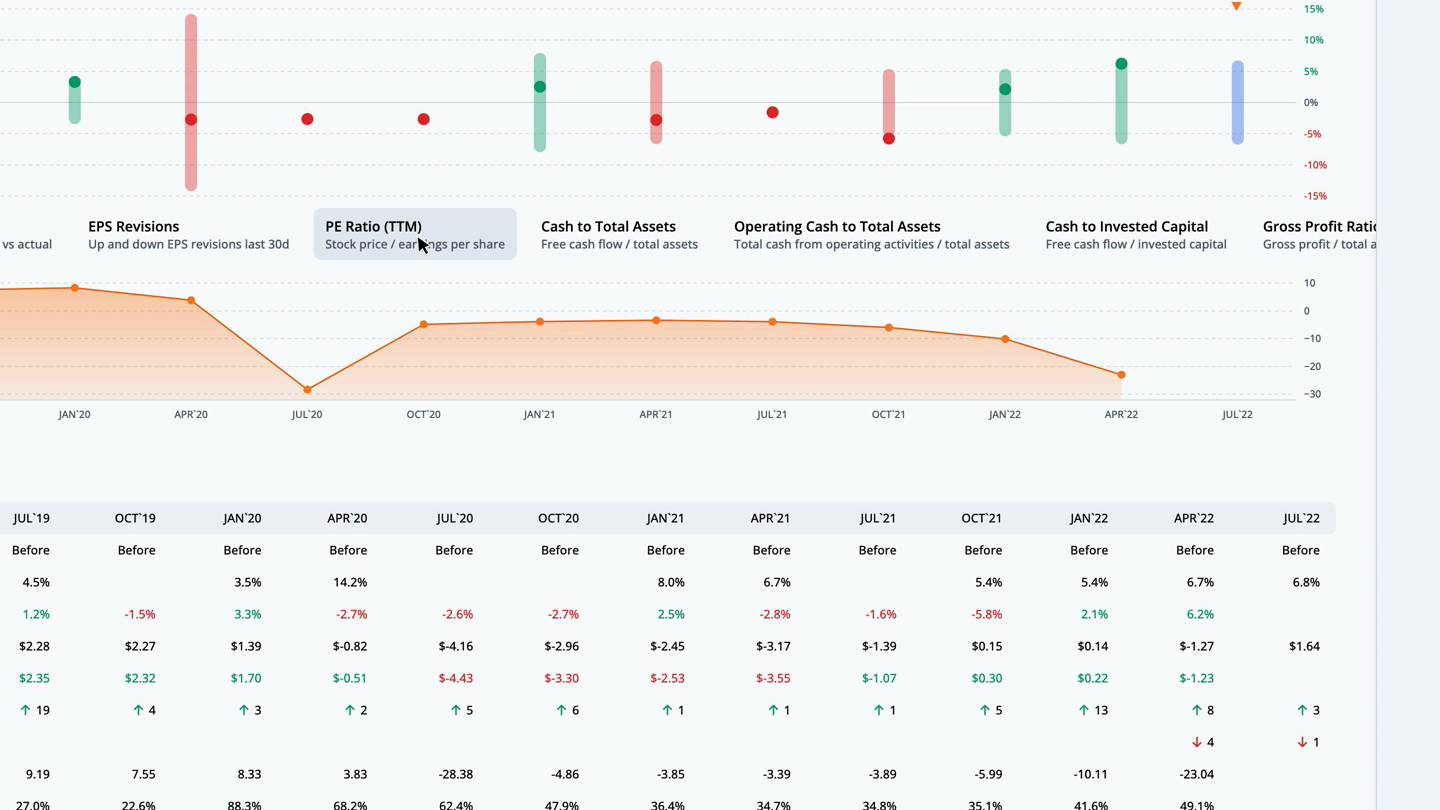

During that time, the post-earnings move was outside of the implied range 1 times. In those cases, long straddles were profitable. The rest of the earnings moves likely yielded profitable short straddles. We can overlay quarterly financial data by clicking on the ratios below the earn move graph. Let’s look at the PE ratio, which is the stock price divided by the trailing twelve months earnings per share.

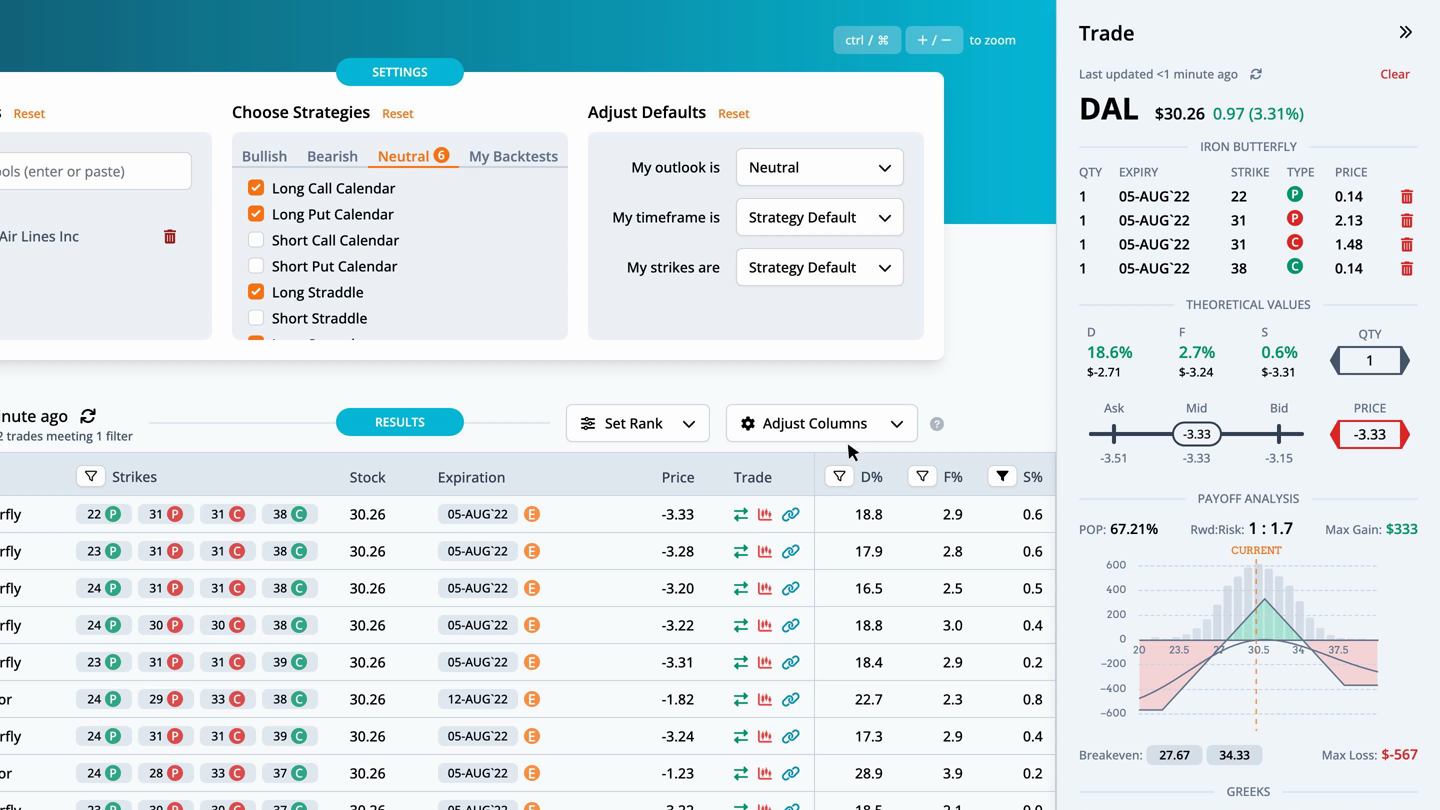

For DAL, the current PE ratio is -17.0, which is 226.9% over the average for the last twelve earnings observations. Returning to the overview tab, we can quickly run a scan to find the best option trades. Since earnings are right around the corner, we scan for neutral strategies, then filter the scan results by S%, or smoothed edge, by setting it between negative and positive 3%.

This helps narrow the results to trades that are fairly priced. The highest ranked trade is a Iron Butterfly with strikes at 22, 31, and 38, expiring on 2022-08-05, for a credit of $3.33.

By pulling up the trade, we can see the theoretical values in more detail. The distribution edge, found by the expected value of the payoff picture on the stock’s historical distribution, has an edge of 18.6%. The forecast edge, which is derived from historical volatility, has an edge of 2.7%. Lastly, the smoothed edge, which is calculated by drawing a best fit curve through the monthly implied volatilities, has an edge of 0.6%. The edge is relative to the mid-market price of the trade. Greater positive edges are a theoretical benefit to the trader. We can also look at the payoff graph.

The probability of profit sums the probability of the nodes for the part of the payoff picture above the zero profit line over three standard deviations. For this trade the probability of profit is 67.21%. The reward to risk divides the max gain by the max loss. Here the 1 to 1.7 is the ratio of the max gain of $333 to the max loss of $-567. There are two break evens for this Iron Butterfly at 27.67 and 34.33. The total greeks and ThinkOrSwim code complete the information on the trade analysis popout.

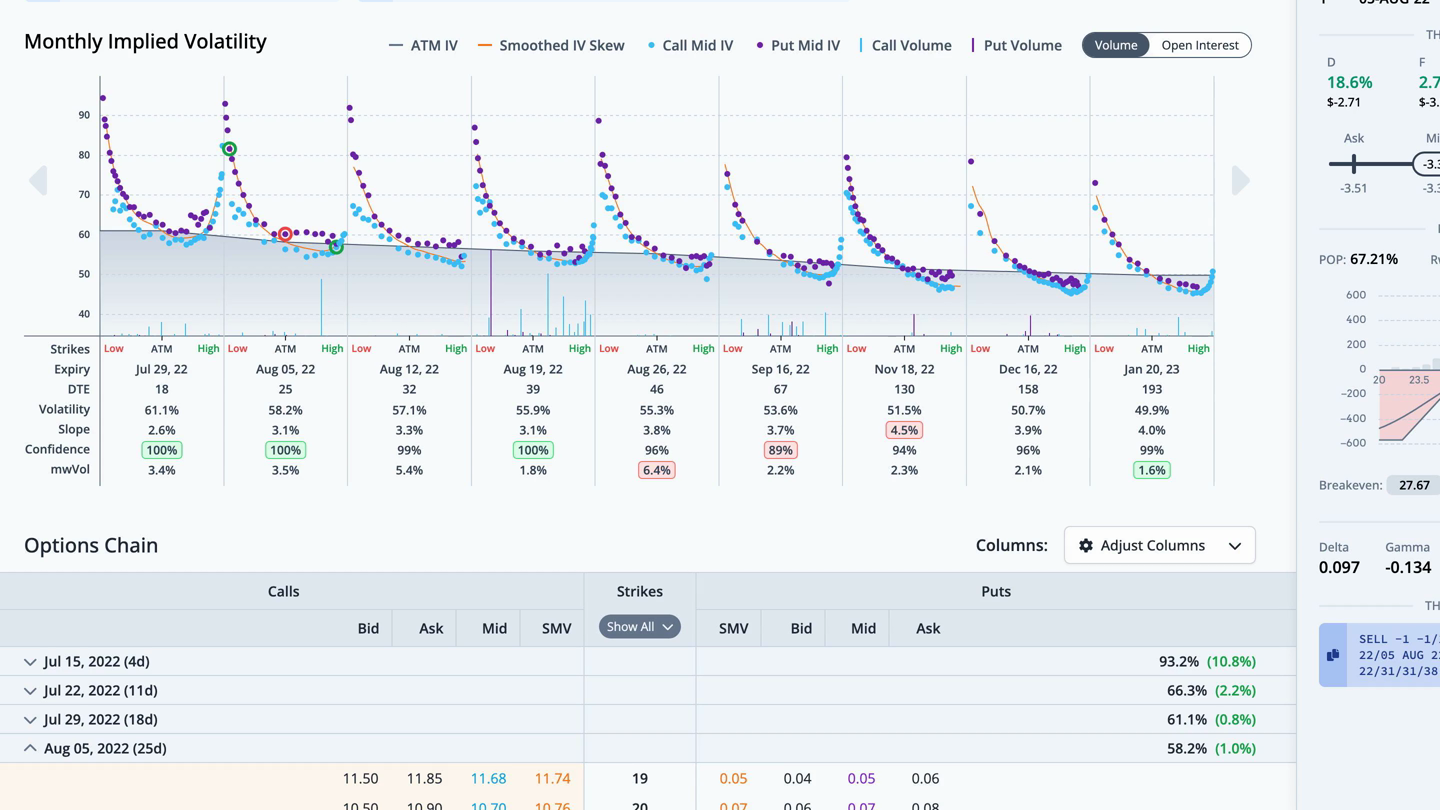

Next, let’s look at this trade in the trade builder. Over the last month, the stock price fell 6.1%, while the thirty-day implied volatility fell 7.1%. The average slope of the trendlines is negative. The heatmap on the right side of the graph is green where volatility and slope are undervalued, and red where they are overvalued. In this case, short term IV and slope are slightly undervalued, while the long term is slightly overvalued.

We can also see this trade overlaid on the monthly implied volatility graph in the chain tab. The legs for this trade are circled. For any questions or issues with the article, please contact otto@orats.com. To subscribe to the dashboard, please visit https://orats.com/dashboard

About the Author: Matt Amberson, Principal and Founder of Option Research & Technology Services. ORATS was born out of a need by traders to get access to more accurate and realistic option research. Matt started ORATS to support his options market making firm where he would hire statistically minded individuals, put them on the floor, and develop research to aid in trading options. He is heavily involved with product design and quantitative research. ORATS offers data and backtesting on a subscription basis at www.orats.com. Matt has a Master’s degree from Kellogg School of Business.

Original source: https://steadyoptions.com/articles/dal-earnings-report-july-13-2022-r704/