A winning ratio is simply a number of winning trades divided by the total number of trades. For example, a trader who won 15 out of 20 trades would have a 75% winning ratio. A 90% winning ratio strategy in options usually refers to Out Of The Money credit spreads that have 90% probability to expire worthless. To achieve a 90% probability, you have to sell credit spreads with short deltas around 10.

Options Delta can be viewed as a percentage probability that an option will wind up in-the-money at expiration. Looking at the Delta of a far-out-of-the-money option is a good indication of its likelihood of having value at expiration. An option with less than a .10 Delta (or less than a 10% probability of being in-the-money) is not viewed as very likely to be in-the-money at any point and will need a strong move from the underlying to have value at expiration.

When you sell a credit spread with short deltas around 10, they have approximately 90% probability to expire worthless. So theoretically, you have a chance to have a 90% winning ratio.

Here is the problem: when you have a 90% probability trade, your risk/reward is terrible – usually around 1:9, meaning that you risk $9 to make $1. Also with 90% probability trades, your maximum gain is usually limited to 8-10%, but your loss can be 100%. That means that you can have a 90% winning ratio, and still lose money. Also consider the fact that if you win 10% five times in a row and then lose 50%, you are not breakeven. You are actually down 25%.

The risk becomes even higher when you sell weekly credit spreads. With closer expiration, the Gamma Risk becomes much higher and the losses start to grow really fast when the underlying goes against you.

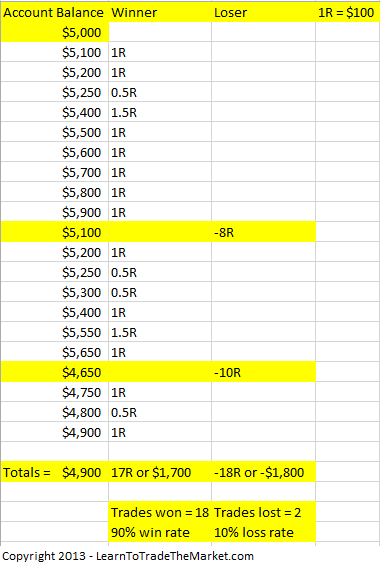

In the example image below, we can see that even with a 90% winning percentage, a trader can still lose money if they take losses that are too large relative to their winners:

It should be obvious by now that a winning ratio alone doesn’t tell the whole story – in fact, it is pretty meaningless.

Here is how Karl Domm describes it:

And the key is this: you may be able to win 80-90% of your trade selling options in a bull or sideways market and even possibly in a grind down market. In fact, you may be able to be profitable in those markets where your average winner with more occurrences outpaces the average loser with the lower occurrences for an overall gain, but what about the crash market?

The last three crashes occurred on August 15,2015; February 5, 2018; and March 2020. This is what your high win rate guru does not want to talk about. They will avoid talking about a crash and they possibly never even experienced the crash or they never back tested their system through a crash. They might not even know what’s going to happen in a crash or they’re just avoiding it altogether on purpose.

Does it mean that credit spreads are a bad strategy? Not at all. But considering a winning ratio alone to evaluate a strategy is not a smart thing to do.

On the other side of the spectrum are traders who completely dismiss credit spreads due to their terrible risk/reward ratio. Here is an extract from an article by an options guru:

The truth is that OTM Credit Spreads have a high probability of making a profit. The average Credit Spread trader will face 100% losses on this trade several times a year while trying to make a modest 5 to 10% a month. What happens is that eventually most Credit Spread Traders meet their doomsday. Sooner or later, virtually all option traders who use only OTM Credit Spreads wipe out their trading accounts.

Let’s look at the “Computer Glitch” of 2010 when the DOW dropped 1000 points in a matter of minutes. Those doing Credit Spreads on this day lost on average between 70% and 90% of their portfolio. What happened is that the volatility rose drastically and the trades moved into that “danger zone” where they lose 100% 10 percent of the time. The Credit Spread trader doesn’t realize that the 10 percent of the time they lose can happen AT ANY TIME. Most people think that they will have 9 wins followed by 1 loss, but this obviously is not how the law of probability works. It’s not uncommon for an OTM Credit Spread trader to face a catastrophic loss on their very first trade, and once this happens, there is no way to recover since a winning trade will only bring back 10% on the remaining capital.”

While I agree that credit spreads are much riskier than most traders believe, the article ignores few important factors. It is true that credit spreads can experience some very significant losses from time to time. But this is where position sizing comes into play. Personally, I would never place more than 15-20% of my options account into credit spreads – unless they are hedged with put debit spreads and/or puts.

Overall, credit spreads and other high probability strategies can and should be part of a well-diversified options portfolio, but traders should concentrate on managing the strategy and the risk, and not on the winning ratio. In fact, many professional traders consider a 60% winning ratio excellent. For example, Peter Brandt admits that his winning ratio is only 43% – yet his Audited annual ROR is 41.6%. Many strategies are designed to have few big winners and many small losers.

The bottom line: the only thing that matters in trading is your overall portfolio return. A winning ratio simply doesn’t tell the whole story.

Related articles:

- Why Winning Ratio Means Nothing

- Selling Options Premium: Myths Vs. Reality

- Gamma Risk Explained

- Why You Should Not Ignore Negative Gamma

- James Cordier: Another Options Selling Firm Goes Bust

- How Victor Niederhoffer Blew Up – Twice

Original source: https://steadyoptions.com/articles/high-probability-strategy-a-holy-grail-of-options-trading-r745/