We will assume you already know that a put credit spread has a positive delta, positive theta, and negative vega.

Today, we will dive deep into how these Greeks change with different configurations of the put credit spread.

Contents

-

-

- Example Greeks Of A Put Credit Spread

- What Happens When We Move A Credit Spread Closer To The Money

- What Happens When We Widen The Width Of A Put Credit Spread

- What Happens When We Move The Credit Spread Further Out In Time?

- Conclusion

-

Questions like:

- How does moving a put credit spread closer to the money affect the delta?

- What happens to theta when the spread is further out in time?

- What happens to vega when we increase the spread width?

Example Greeks Of A Put Credit Spread

Here is an out-of-the-money put credit spread on SPY that is 41 days out in time.

Sell one contract Feb 7, 2025, SPY $565 put at $3.09

Buy one contract Feb 7, 2025, SPY $560 put at $2.62

Net credit: $47.50

Max loss: $452.50

Risk-to-reward: 9.5

The delta of the long $560 put option is -13, and the delta of the short $565 put option is 16.

Thus, this spread has its short option at the 16 delta.

A long put has a negative delta because it benefits if the underlying price goes down.

A short put has a positive delta because it benefits if the price goes up.

When we combine the two legs, the Greeks for the bull put credit spread on a per contract basis are:

Delta: 2.7

Theta: 0.66

Vega: -5.46

Gamma: -0.11

The overall positive delta shows that the spread has a bullish directionality.

The positive theta shows that this spread benefits from the passage of time.

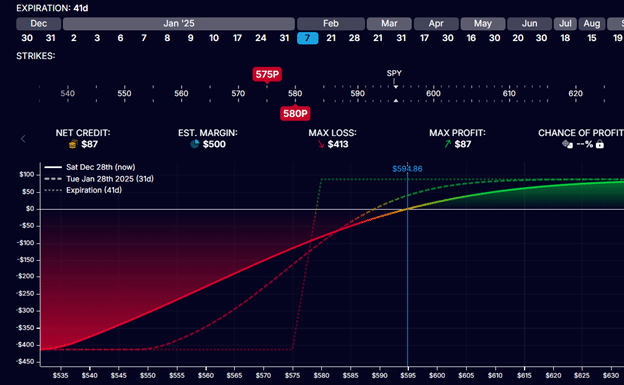

What Happens When We Move A Credit Spread Closer To The Money

If this same 5-point-wide spread was placed closer to the money with the same expiration, we have:

Initial credit: $87

Max Risk: $413

Risk-to-reward: 4.7

A closer to the money spread gives a bigger initial credit.

This is why you will get a credit for this roll when you roll a spread closer to the money (while keeping the spread width and expiration the same).

Because of the larger credit (with the same spread width), we have decreased the maximum risk of spread (from $452.50 to $413).

And thereby reducing the risk-to-reward ratio.

Let’s look at the Greeks.

Delta: 4.70

Theta: 0.40

Vega: -5.95

Gamma: -0.16

Moving the spread closer increased the directionality of the spread (larger delta) and increased gamma (the rate of change of delta as the price of SPY moves).

A spread closer to the money will have less time decay, as indicated by a smaller theta.

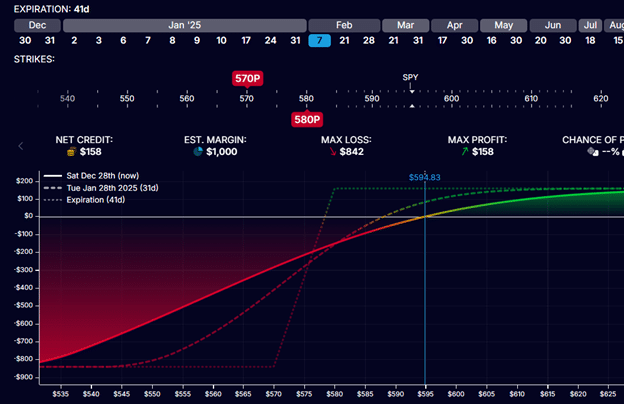

What Happens When We Widen The Width Of A Put Credit Spread

If we were to widen the width of the credit spread to 10 points, as in:

We would receive a larger credit for a larger risk, increasing the risk-to-reward slightly:

Credit: $158

Max risk: $842

Risk to reward: 5.3

How did the Greeks change?

Delta: 8.60

Theta: 0.93

Vega: -11.96

Gamma: -0.31

We have increased the directionality of the spread and its gamma even more.

And the magnitude of vega has increased.

At least we have now bumped up theta because the long protective leg of the spread less impedes theta.

When we keep increasing the width of the spread more and more, it starts to behave more and more like a single short put (closer to that of an undefined risk position).

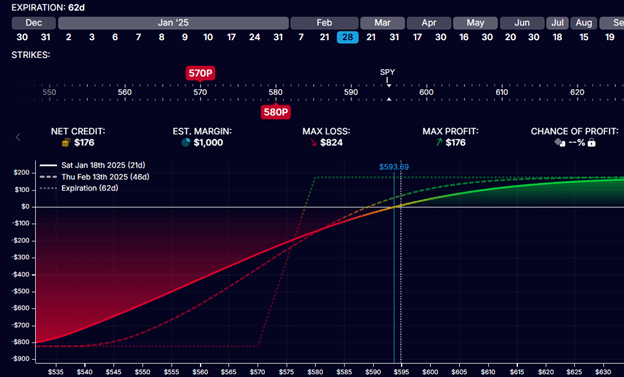

What Happens When We Move The Credit Spread Further Out In Time?

We will keep the same strikes at $580 and $570 but place the spread at a later expiration (such as Feb 28, two weeks later).

We get an even larger credit because we are selling more extrinsic value.

Credit: $176

Max risk: $824

Risk to reward: 4.6

When a credit spread is not working out or getting too close to expiration, some traders will like to roll the spread to a later expiration.

This means closing out the existing spread and opening a new spread with the same width at a later expiration date.

Ideally, they will want to get a credit for this adjustment.

This means that the initial credit of a new spread needs to be larger than it costs to close the existing spread.

If they can get this without changing the spread width, they would increase their credit and thereby reduce their max risk.

The max risk in a credit spread is the width of the spread minus the credits received.

Let’s look at the Greeks, who are further dated and spread two months out in time.

Delta: 7.91

Theta: 0.39

Vega: -11.58

Gamma: -0.23

The magnitude of every Greek decreases.

The Greeks are less strong further out in time.

Conclusion

Knowing the Greeks of a credit spread is important in initial placement and in adjusting.

A trader who is confident in the market direction may place a spread closer to the money for greater directionality.

A trader mainly interested in collecting premiums from time decay may want to place the spread further away from the money for the increased theta.

A trader who doesn’t have time to check the markets often may want to place the spread further out in time.

Because the delta will not change so much since the magnitude of gamma is lower.

When a credit spread approaches expiration, gamma increases.

If this gamma is too much, a trader may roll the spread out in time to reduce the gamma.

A trader may also roll the spread further out in time if the spread is being threatened, with the price coming closer to the short strike.

As long as the trader keeps the spread width the same and collects a credit for the roll, this decreases the maximum risk in the trade.

It also decreases the directionality of the spread (delta is lower).

If a trader trades two out-of-the-money credit spreads (as in an iron condor), he may roll the un-threatened spread closer to the money to collect additional credits.

Remember that an out-of-the-money credit spread (whether put or call spreads) will collect additional credit when you roll it closer to the money.

This additional credit offsets the maximum risk of the trade (as long as the width of the spread remains the same).

Certain spread configurations may be “better” for one trader but not for another.

Options are usually fairly priced.

So if you think, “Hey, look at how much more credit I can get for this spread over the other one.”

You need to ask what you are taking on or giving up to get this credit.

If you move your spread closer to the money, yes, you get more credit, but you are taking on more directional risk.

If you move your spread further out in time, you get more credit, but you now have less theta.

If you think trying to get the largest theta is the “best,” think again.

Yes, you can get more theta by moving the spread closer to expiration, but now you are taking on directional risk (larger delta) and gamma risk (larger magnitude of gamma).

You can then say, “Well, I’ll move my spread far out of the money.”

Then I have low delta and low gamma but still somewhat high theta.

Yes, that configuration focuses on capturing income from time decay.

However, its risk-to-reward ratio is not as good as the other configurations.

We hope you enjoyed this article on the options Greeks of a put credit spread.

If you have any questions, please send an email or leave a comment below.

Trade safe!

Disclaimer: The information above is for educational purposes only and should not be treated as investment advice. The strategy presented would not be suitable for investors who are not familiar with exchange traded options. Any readers interested in this strategy should do their own research and seek advice from a licensed financial adviser.

Original source: https://optionstradingiq.com/options-greeks-of-a-put-credit-spread/