Discover how selling in-the-money covered calls can reduce your stock position risk without selling shares.

Learn the mechanics of delta reduction, assignment risks, tax considerations, and when ITM call overwriting makes sense as a hedging strategy.

Contents

-

- What You’re Really Doing When You Sell An ITM Call

- Key Things To Consider Before Selling ITM Calls

- 1. How Much Upside Are You Willing To Give Up?

- 2. Assignment Risk

- 3. Tax Considerations

- 4. Impact On Delta (Exposure)

- 5. Premium Vs Protection

- Pros And Cons Of ITM Call Hedging

- Additional Strategic Considerations

- ITM Calls Vs Other Hedging Strategies

- Real-World Example

- FAQs About Hedging With ITM Calls

- Conclusion: Know What You’re Trading

What You’re Really Doing When You Sell An ITM Call

Most traders think of covered calls as an income strategy—selling out-of-the-money calls to generate premium.

But selling in-the-money (ITM) calls serves a different purpose: it’s a hedging tool that reduces downside exposure.

The Concept

Long stock + Short ITM call ≈ Short put (synthetically)

You’re hedging by giving up upside in exchange for premium and downside buffering.

Example

You own 100 shares at $100:

Without a hedge:

- Stock drops to $90: Lose $1,000

- Stock rises to $110: Gain $1,000

Sell $90 ITM call for $11.00:

- Collect $1,100 premium

- Net delta drops from +100 to approximately +15

- Stock drops to $90: Lose $1,000 on stock – $1,100 premium = net loss only $100 (vs $1,000)

- Stock rises to $110: Capped at $90 strike

The trade-off: You’ve reduced downside risk by 90%, but capped upside at $90.

Learn More About Covered Call Strategies

Download Free Options Trading Resources – Explore systematic approaches to covered calls and hedging.

Key Things To Consider Before Selling ITM Calls

Before implementing this strategy, you need to understand several critical factors that will determine whether it’s right for your situation.

1. How Much Upside Are You Willing To Give Up?

This is your biggest decision.

Strike Selection Framework:

Stock at $100, your choices:

Deep ITM ($85): Maximum protection, very tight upside cap

Moderately ITM ($90): Balanced protection and participation

Slightly ITM ($95): Light protection, reasonable upside

Choose based on your concern level about downside versus desire for upside participation.

2. Assignment Risk

ITM calls carry a real chance of early assignment—especially:

- Near ex-dividend dates

- When extrinsic value drops near zero

- Deep ITM with little time premium

What This Means:

- You may lose your shares unexpectedly

- Potential unwanted tax consequences

- Need to repurchase if you want to keep the position

Example: Sold a $90 call on a $100 stock.

Stock hits $105, call trades at $15.10 (only $0.10 time value).

Buyer exercises early.

You’re forced to sell at $90 while the stock is at $105.

How to Manage:

- Monitor extrinsic value closely

- Roll when the time value drops below $0.30-$0.50

- Avoid holding through ex-dividend dates

- Close position if the assignment is unacceptable

3. Tax Considerations

Tax implications vary by jurisdiction.

Key concerns:

Assignment Triggers Capital Gains:

- Forces realization of gains/losses

- Timing may not align with your tax planning

Cost Basis Issues:

- Repurchasing resets cost basis

- Lose a long-term holding period built up

Example: Bought at $50, now $100, held 11 months. Sell $90 ITM call.

If assigned before 12 months, realize short-term (vs long-term) capital gains—potentially doubling your tax rate.

Recommendation: Consult a tax professional for sizable positions.

Tax implications can significantly impact net results.

4. Impact On Delta (Exposure)

This is why people use this strategy.

The Math:

- Stock delta: +1.00

- Sell call with delta: -0.85

- Net delta: +0.15

You’ve cut 85% of directional risk while keeping shares.

Practical Impact (100 shares at $100):

Before: Stock moves $5 → You gain/lose $500

After (0.85 delta call): Stock moves $5 → You gain/lose ~$75

This tempers volatility but doesn’t eliminate it.

5. Premium Vs Protection

ITM calls provide premium (intrinsic + time value), creating a two-part hedge:

- Premium received – Immediate buffer

- Reduced delta – Ongoing risk reduction

Stock drops: Premium softens blow, reduced delta means smaller losses.

Stock rises: Can’t participate beyond strike, keep premium

The core trade-off: “I’ll cap upside to reduce downside and collect premium now.”

This is risk reduction, not elimination.

A 50% stock collapse still hurts—you just lose less.

Pros And Cons Of ITM Call Hedging

Understanding both sides helps you decide if this strategy fits your situation.

Pros

✓ Reduces Delta Without Selling Shares

You maintain ownership while cutting directional exposure by 50-85%+.

✓ Brings in Premium to Soften Downside

The premium acts as a buffer, reducing losses if the stock declines.

✓ Simple to Manage Mechanically

It’s just selling covered calls—a straightforward options trade that most brokers support.

✓ May Avoid Triggering Tax Events

You don’t sell shares, so you don’t immediately realize capital gains (unless assigned).

✓ Works Well in High IV Environments

When implied volatility is elevated, you collect more time premium, making the hedge more attractive.

✓ Can Be Adjusted as Thesis Changes

Roll up, down, or out to different strikes and expirations as your outlook evolves.

Cons

✗ Caps Upside—Sometimes Aggressively

If the stock rallies 30%, you might only capture 5-10%, depending on your strike selection.

✗ Early Assignment Risk

ITM calls can be assigned early, forcing you to sell shares at potentially inopportune times.

✗ Still Carries Downside Exposure

Unless you go extremely deep ITM, you’re not fully protected. A 30% drop still hurts.

✗ Rolling Deep ITM Calls Can Be Awkward

Wide bid-ask spreads and sticky intrinsic value make adjustments more expensive.

✗ Tax Implications

Assignment triggers capital gains. Holding period resets if you repurchase. Wash sales may apply.

✗ Not a Perfect Hedge

If the stock collapses, your hedge isn’t perfect—you lose less than you would have unhedged.

Additional Strategic Considerations

Define Your Goal

Common objectives:

- Hedge through a specific event (earnings, Fed announcement)

- Reduce exposure for 1-3 months during uncertainty

- Lower portfolio volatility temporarily

Time Horizon

Short-term (1-3 months): Near-term expiry works well

Long-term (6+ months): Protective puts or collars may be cleaner

Have Clear Rules

Decide in advance when you’ll:

- Roll up (stock rises, want more upside)

- Roll down (stock falls, need more protection)

- Close hedge (concerns dissipate)

- Convert to a different structure (collar, put spread)

Compare Alternatives

Always evaluate against: protective puts, put spreads, collars, position reduction, or doing nothing.

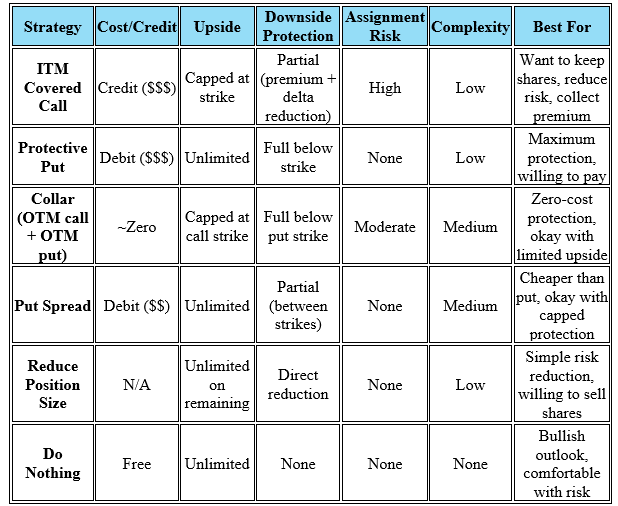

ITM Calls Vs Other Hedging Strategies

Here’s how selling ITM covered calls compares to other common hedging approaches:

Key Takeaways:

- ITM calls are unique in collecting a credit while providing partial protection

- Protective puts offer the cleanest downside protection, but cost money

- Collars balance cost and protection, but cap both upside and downside

- Position reduction is simplest but triggers tax events immediately

Real-World Example

Situation: You own 200 shares purchased at $80, now at $120 ($8,000 unrealized gain).

Earnings next week.

Don’t want to sell for tax reasons.

Action: Sell 2 contracts of $115 call (slightly ITM) for $8.00, expiring in 30 days.

Setup:

- Premium collected: $1,600

- Delta reduction: +200 to +60 (70% reduction)

- Upside capped at $115

Outcome 1 – Stock drops to $105:

- Stock loss: -$3,000

- Premium kept: +$1,600

- Net loss: -$1,400 (vs -$3,000 unhedged)

- Hedge reduced loss by 53%

Outcome 2 – Stock rises to $135:

- Can only capture up to a $115 strike

- Called away at $115 vs $120 purchase = -$1,000 opportunity cost

- Premium kept: +$1,600

- Net: +$600 (vs +$3,000 unhedged)

- Gave up $2,400, but achieved goal: protection through earnings

Lesson: The hedge worked as designed—reducing downside significantly while capping upside participation.

FAQs About Hedging With ITM Calls

What does selling an ITM covered call do to my position?

Selling an ITM covered call reduces your directional exposure (delta) by 50-85% while collecting premium.

You keep shares but give up upside above the strike in exchange for downside buffering.

Example: Own stock at $100, sell $90 ITM call with 0.80 delta—your net delta becomes +0.20 instead of +1.00.

When should I use ITM calls instead of protective puts?

Use ITM calls when you want to collect premium (credit) rather than pay for protection (debit), and you’re comfortable capping upside.

Choose protective puts when you want full downside protection while keeping unlimited upside, and you’re willing to pay for that insurance.

What’s the biggest risk of selling ITM calls?

Early assignment—especially near ex-dividend dates or when extrinsic value drops near zero.

This forces you to sell shares at the strike price, potentially triggering unwanted capital gains taxes and removing your position before your intended time.

You also face opportunity cost if the stock rallies significantly above your strike.

How do I avoid early assignment on ITM calls?

Monitor extrinsic value closely and roll when time value drops below $0.30-$0.50.

Avoid holding through ex-dividend dates if you want to keep shares.

Don’t sell calls too deep ITM where assignment is almost certain.

Close the position before expiration if keeping shares is critical.

Should I sell ITM calls or reduce my position size?

Sell ITM calls when you have tax or strategic reasons to keep shares (avoiding capital gains, maintaining long-term holding period).

Reduce position size when you want less exposure without tax concerns.

ITM calls provide more flexibility but require more active management.

How does implied volatility affect ITM call hedging?

Higher implied volatility makes ITM call hedging more attractive because you collect more time premium on top of intrinsic value.

In high IV environments, you get better compensation for giving up upside.

In low IV, there’s less time premium, reducing the strategy’s appeal.

Conclusion: Know What You’re Trading

Selling ITM calls can be effective for hedging, but only when you understand:

- The protection-upside trade-off

- Assignment implications

- Delta shift impact

- Purpose and time horizon

- Tax consequences

Is This Right for You?

Use ITM calls when:

- You have tax/strategic reasons to keep shares

- Concerned about near-term downside (not catastrophic drops)

- Comfortable capping the upside

- Want to collect premium while reducing risk

Use alternatives when:

- Need maximum protection (buy puts)

- Can’t tolerate assignment (use put spreads)

- Long hedge timeframe (collars better)

- Simply want less exposure (reduce position)

Not “Set and Forget”

This requires active management:

- Define your goal

- Choose appropriate strikes

- Monitor assignment risk

- Have adjustment rules

- Understand tax implications

Final thought: ITM call hedging says, “I want to temporarily reduce exposure without selling.”

If that’s your situation and you understand the trade-offs, it’s a powerful risk management tool.

But, as with all hedging, it involves costs—in this case, giving up upside and facing assignment risk.

Related Articles

- Selling Put Options Strategy

- The Wheel Strategy

- Bull Put Spreads Guide

- Best Iron Condor Strategy

- Weekly Option Strategies

We hope this guide helped clarify how to use ITM covered calls as a hedging strategy.

If you have any questions, please send an email or leave a comment below.

Trade safe!

Disclaimer: The information above is for educational purposes only and should not be treated as investment advice. The strategy presented would not be suitable for investors who are not familiar with exchange traded options. Any readers interested in this strategy should do their own research and seek advice from a licensed financial adviser.

Original source: https://optionstradingiq.com/selling-itm-calls-to-hedge-stock/