The JPM Collar is a recurring options strategy used by a major institutional investor whose position is so large that it has become somewhat well-known in the options world.

It has been speculated that it can influence short-term market flows in the S&P 500 options complex.

Contents

- How It All Began

- Construction Of The JP Morgan Collar

- Volatility Skew Of SPX

- Rolling The Collar

- Historical Performance Of The JPM Collar

- Does It Affect The Retail Investors?

- Final Thoughts

How It All Began

JPMorgan has a fund called the JPMorgan Hedged Equity Fund (JHEQX).

The fund typically holds around 150 large-cap equities, including many well-known blue-chip names such as Nvidia, Apple, Microsoft, Amazon, Alphabet, Meta, Broadcom, Tesla, and Mastercard.

The term “hedged” reflects the fund’s built-in downside protection, designed to help cushion the portfolio during sharp market sell-offs or black swan events.

To achieve this protection, the fund uses an options collar strategy.

A collar is when an investor who already owns equities buys a protective put to protect the fall of those assets.

To help finance the cost of the put option, the investor sells a call option to generate some premium.

This allows the investor to hedge the downside at a reduced net cost.

Construction Of The JP Morgan Collar

Not everyone realizes that JPMorgan uses a specific variant of the collar strategy, partly because most investors and even many AI agents never read the fund’s brochure or fact sheet.

The fund employs a zero-cost put-spread collar.

It buys an out-of-the-money (OTM) put option at 5% below the current SPX price and sells a put option at roughly 20% below.

This creates a put spread that begins protecting the portfolio after a 5% decline and continues offering protection until around a 20% drop.

Beyond that point, losses resume because the spread no longer provides coverage.

Using a put spread instead of a single long put significantly reduces the cost of the hedge.

On the upside, the fund sells a call spread at a level designed to collect enough premium to offset the cost of the put spread, making the overall collar nearly cost-free.

In practice, the short call strike typically ends up about 3% to 5% above the current SPX level.

Below would be the resulting payoff diagram, showing the combination of the put spread and the short call layered on top of the underlying equity holdings.

The premium from selling the call options pays for the put debit spread hedge.

The tradeoff is that it caps the upside.

While the downside losses can still be unlimited in very rare circumstances, the collar offers meaningful downside protection under most realistic market environments.

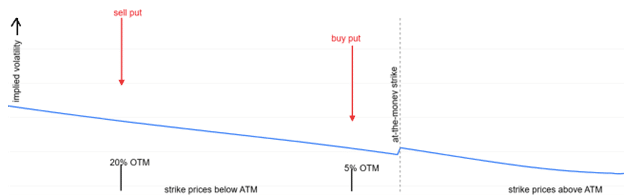

Volatility Skew Of SPX

Another advantage of using a put spread is that it naturally benefits from the smirk-shaped volatility skew in the SPX, creating a steep downward slope in IV across strikes.

Lower-strike puts trade at higher implied volatilities than higher-strike puts.

This is an advantage because the spread is selling at a higher IV and buying at a lower IV.

Rolling The Collar

The collar is established at the beginning of each quarter and runs for the entire three-month period.

It typically uses options that expire on the quarterly expiration date.

Once in place, the position is left untouched and held through to expiration without any adjustments.

They roll to a new collar on the last day of the existing collar.

What time do they roll?

Well, that is up to them.

But it is coordinated so that there is not a large intraday delta risk.

They put on the new collar and just let the old collar expire.

Therefore, there is time during the day when both collars are active.

This double hedging results in a large, undesirable negative delta.

So when they put on the new collar, they also put on enough 0-DTE call options to balance that delta back to its norm.

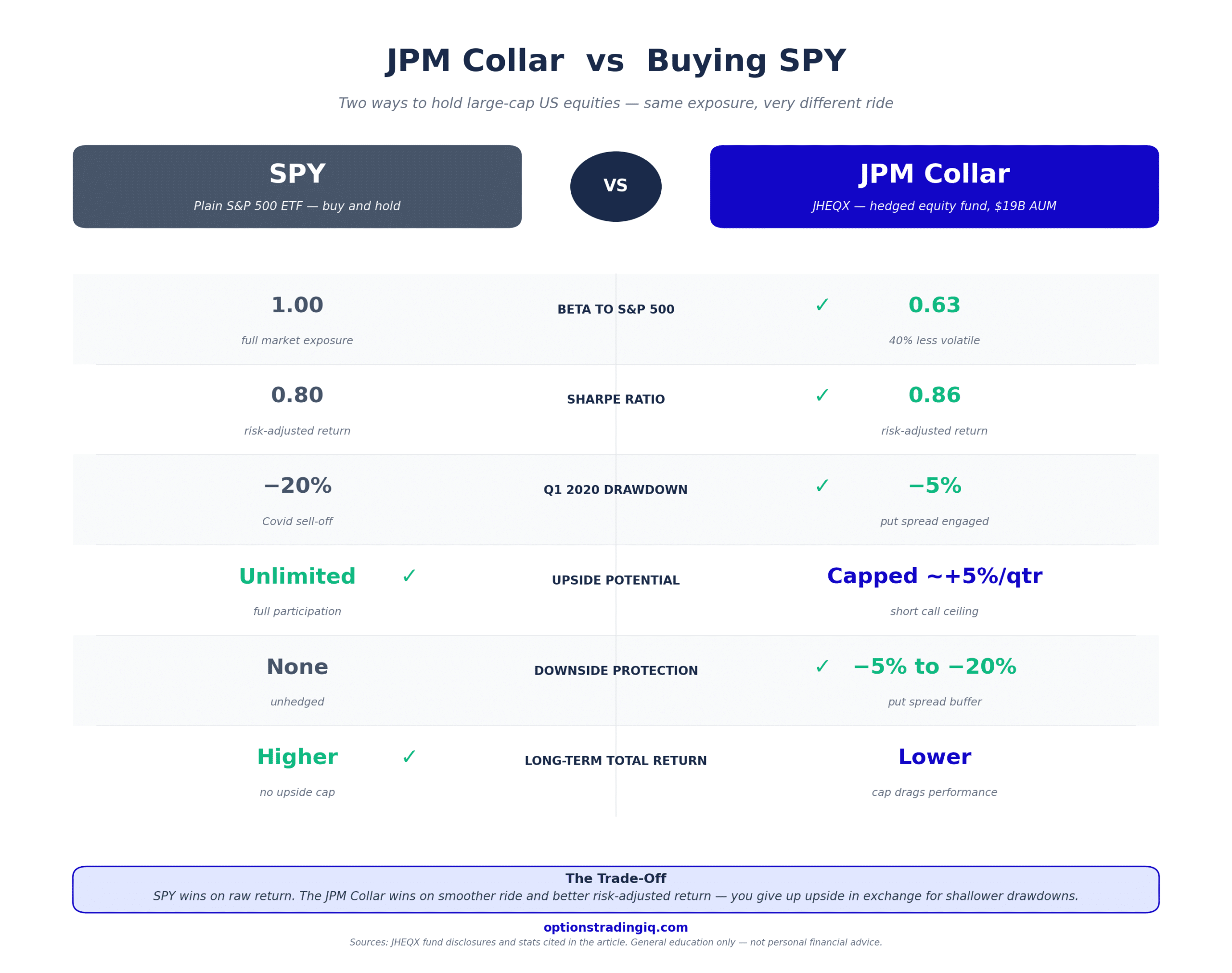

Historical Performance Of The JPM Collar

Since the fund’s inception in 2014, it has underperformed the S&P 500 due to the upside cap imposed by selling call options.

The blue line is SPX, and the candlestick graph is the JHEQX fund.

The benefit is that the collar overlay reduces the volatility (the number of up-and-down swings) in the fund’s value.

The fund has a beta of 0.63 and is 40% less volatile than the S&P 500.

Many investors are willing to accept a lower return to reduce risk and achieve lower drawdowns.

This also means that the fund managers can sleep better at night, knowing that 19 billion dollars in assets under management are somewhat protected.

Since inception, the put spread had come into play four times, where the underlying asset price dipped below the long put strike – years 2015, 2018, 2020, and 2022.

Taking the Covid pandemic drawdown as an example, SPX was down 20% for the first quarter of 2020 while the JHEQX was down only 5%.

Since the collar reduced the impact of large losses, JHEQX’s risk-adjusted returns are actually slightly better than SPX’s.

The fund has a Sharpe ratio of 0.86, compared with 0.80 for SPX.

Does It Affect The Retail Investors?

Due to the fund’s massive size, which often requires 40,000 contracts.

Market makers that need to take the opposite side of this large position have large gammas at the JPM call strike and at the long put strike.

This can cause “gamma pinning” of SPX to these levels near expiration, which are especially noteworthy to zero-DTE traders, where these effects are most pronounced.

Second-order Greeks also become relevant in a position of this size, whereas they would barely matter in smaller trades.

As the JPM Collar gets closer to expiration, these effects force market makers to adjust their hedges.

Charm is the second-order Greek that measures how an option’s delta changes over time.

It causes out-of-the-money options to lose delta and in-the-money options to gain delta, even if all other market factors remain unchanged.

Vanna is another second-order Greek that causes delta changes when implied volatility changes.

Whenever delta changes, market makers need to buy or sell stock or futures to maintain their neutral position.

The quarterly reset and re-positioning on the final business day often trigger intense market volatility with market makers hedging around these large strikes.

Once the position is rolled, the immediate hedging pressure dissipates, typically reducing short-term volatility.

Final Thoughts

The JPM collar’s massive scale can affect the options’ implied volatility surface as expiration nears.

Certainly, even retail traders can see how the JPMorgan position is positioned by looking at option volume, open interest, and GEX signatures.

During the most recent collar expiration on March 31, 2026, the JPM long put strike was at 6475 on the SPX.

A week before expiration, a large negative GEX can be seen at that strike.

Looking at 15-minute candles on SPX…

We see that the market tested that level on March 20 and closed very near that strike on March 26.

On the expiration day of March 31, the large green 15-minute candle zoomed up through the 6475 strike during the New York lunch hour.

Was that when the collar was rolled?

Was the JPM Collar at play?

Or coincidence?

We hope you enjoyed this article on the JPM collar.

If you have any questions, please send an email or leave a comment below.

Trade safe!

Disclaimer: The information above is for educational purposes only and should not be treated as investment advice. The strategy presented would not be suitable for investors who are not familiar with exchange traded options. Any readers interested in this strategy should do their own research and seek advice from a licensed financial adviser.

Original source: https://optionstradingiq.com/jpm-collar-trade/